Risky Business

August 4, 2016 2:26 pm | Posted in Opinions | Share now TwitterFacebook

De-risking is a threat to Vanuatu’s economy. But can we stop it?

Financial jargon seems to serve much the same purpose as military jargon: Hide the damage behind the blandest possible expression. ‘De-risking’ follows that time-honoured tradition. It sounds innocuous enough— after all who likes risk?

But it becomes more ominous when we realise we’re the risk.

Since the late 1990s, richer nations began to realise that globalisation came at a cost. Corporations and individuals took advantage of easy money flows to move their earnings into the most favourable jurisdictions.

This was fine, right up until people began counting tax revenue losses. Between 2001 and 2010, the Internal Revenue Service estimates that the United States economy lost $3.09 trillion due to tax evasion. (That’s ‘evasion’, not avoidance.)

In the wake of the September 11, 2001 terrorist attacks, the United States and other western nations redoubled their efforts to curtail illicit flows of cash as they tried to stamp out terrorist activity. And the 2007 global financial crisis only added to the chorus of voices calling for more accountability in the financial system.

In 2016, HSBC, a multinational banking and financial services company, was hit with nearly US$2 billion in fines. The Guardian newspaper reported that the US government accused the bank of flouting money-laundering laws and knowingly aiding Mexican drug cartels. The company also assisted pariah nations such as Libya, Burma, Sudan and Iran to access the US financial sector. Authorities said the scheme had gone on for decades.

HSBC avoided criminal penalties only because UK Chancellor of the Exchequer George Osborne wrote to his US counterparts, warning them that criminal charges could destroy the bank, and bring the rest of the financial establishment down with it.

The baby and the bath water

The writing was on the wall. With authorities around the world piling up the penalties for bad behaviour, and with groups like the OECD banding together to build transparency and accountability into the global financial system, banks began to reassess the company they kept.

The Financial Action Task Force, or FATF, is an international money laundering and terrorist finance watchdog. In recent years, it has formalised what it calls a Risk Based Approach to countering illegal cash flows.

In a nutshell, an RBA, as it’s known, is one in which authorities and institutions are able to ‘identify, assess and understand’ the risks they’re exposed to. One RBA manual suggests three levers an institution can pull to reduce risk: Knowing your customer, Monitoring activity and Controlling the products you sell.

This makes perfect sense: If you don’t know who’s giving you money, you’d be hard pressed to tell whether it’s good or bad. If you don’t watch what’s happening, then you can’t tell when someone’s playing fast and loose with the rules. And lastly, if you don’t sell dodgy financial products in the first place, you make it harder for your customers to do dodgy things with them.

But problems arise once these principles are put into practice. Very large banks and financial service companies doing business across borders often have vast numbers of products, customers and services. They have neither the time nor the patience to weed through every single account looking for the one that might cost them billions in fines.

A report published by the UK’s financial regulator, the Financial Conduct Authority, outlines the problem. A stricter—and less profitable—global financial environment, “has caused banks to deleverage, and has also created a tougher environment in which to maintain profitable relationships. As a result, many banks have undertaken a strategic review of their business and functions, often choosing to focus on their ‘core’ business.”

In their newfound risk aversion to illegal activity, banks seem to be throwing out the baby with the bathwater: “Banks appear to weigh up a variety of benefits and costs of maintaining an account that are not always related to the financial crime risks the customer might pose.”

The report gives examples: “In one bank, of the 2,500 charity bank accounts closed in 2014 only 59 were closed for reasons that might relate to compliance concerns, and one large bank said that only 0.013% of all its overall small business accounts had been closed for ‘AML linked reasons’.”

That’s a lot of bathwater.

Last resorts

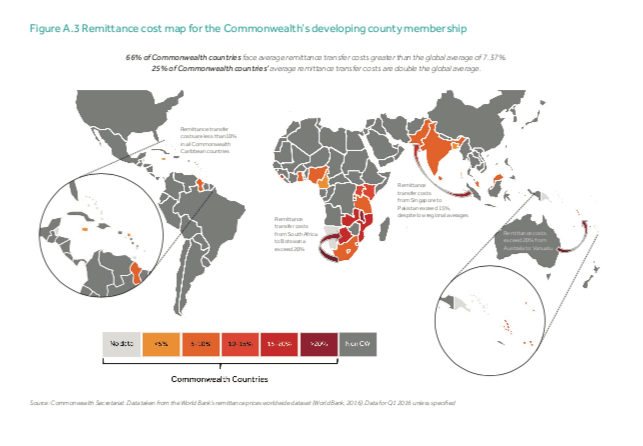

A recent Commonwealth report makes it clear that Caribbean and Pacific island tax havens are suffering significantly as a result. The report cites one expert who claims, “Our research shows a really worrying rise in CBR [correspondent account] closures, doubling year on year since 2013. This is particularly detrimental to the vulnerable economies and small states of the Commonwealth, because it means they simply do not have access to essential facilities such as loans, credit and international money transfers.”

Correspondent accounts are critical to the health of Vanuatu’s economy. Without them, we lose the ability to easily transfer cash in and out of the country.

Samoa relies on remittances for nearly 20% of its GDP. In 2014, transfer fees for remittances ate up about 2% of GDP. The Commonwealth report states: “Between 2013 and 2015, 9 of Samoa’s 15 licensed MSBs [money service businesses] faced account closures in Australia and New Zealand. One Samoan MSB was forced to cease operating in New Zealand as a result….”

The Samoan government was reduced to ‘last resort measures’, including the establishment of its own centralised financial ‘clearing house’. The central bank opened its own accounts, and allowed MSBs to funnel their flows through them. The result was costly, timeconsuming and ungainly, but it staved off outright economic disaster.

The prospects for some tax havens are dire. The Commonwealth report cites a Moody’s study, which paints a dismal picture: “’80% of Belize’s banking system is likely to lose correspondent and credit card settlement services by mid-year 2016‘, with the loss of these services potentially disastrous for the country – compounding existing economic and fiscal frailties, such as depleted oil reserves, impending fiscal imbalances and the planned abolition of EU sugar quotas. Furthermore, if this trend continues, it could place significant pressure on central bank reserves, leading to potential credit default.”

Global redlining

The biggest problem with the global de-risking trend is the way risk is defined. One of the most common criteria used to determine risk is the jurisdiction from which the money originates. Banks are increasingly inclined to tar entire countries with the same brush. And with countries as small as ours, it doesn’t take a very big brush.

The result is a practice that begins to look a lot like the infamous practice of redlining in the USA: Banks simply decided that entire neighbourhoods were not worth lending to, based solely on the colour of their inhabitants. Cutting off an entire nation might be justified if it’s North Korea or Iran, but if we don’t succeed in making good on our efforts to get off the OECD money laundering grey list, we might find ourselves getting the same treatment.

The danger can’t be overstated. There is always a degree of herd behaviour to these situations. If one bank begins closing its Vanuatu CBRs, it could easily lead other banks doing the same. Such a cascade could land us in the same situation as Belize.

But no matter how well we do, it might not be enough. Without the intervention of the OECD, the Commonwealth and other international bodies, we might find ourselves cut off from the global financial community just because we’re not big enough to matter.

Vanuatu needs to clean up its own financial house. But it needs to push back, too. We need to develop a voice on the international stage, one that calls for a fair shake from financial institutions.

If we don’t, our economy might well get de-risked out of existence.