WORLDWIDE BANKING CRISIS?

May 30, 2020 8:00 am | Posted in Features | Share now TwitterFacebook

Vanuatu Banks have been a critical and important part of how businesses affected by the Economic crisis created by COVID-19 are managing their situation. When we run out of money, we turn to our banks for help.

However, we need to also understand that our banks are just another business in Vanuatu. Banks are basically traders of money. In a very simplistic model, they accept deposits from people and institutions who may have funds to invest, offer interest rate returns on these funds and then lend them out again to borrowers. The difference is their margin and this is called the interest rate spread. Banks manage their lending policies based upon their risk appetite which is reflected in the interest rates they charge. The higher the risk, the higher the rate of interest charged to Borrowers. Just like what is happening in Vanuatu, banks worldwide are currently deeply involved in assisting their clients manage the business crisis. At the moment, they are probably too busy dealing with everyday problems of their customers, but those who may be farsighted would see that there are bigger problems post COVID-19.

There is no doubt that there will be casualties as a result of COVID-19. Businesses will close, some for good. The predicament facing banks is a sensitive issue. When customers are desperately needing liquidity to pay bills, wages and other commitments, but have exhausted all their bank facilities, they will invariably request further assistance from their Banks. In Vanuatu, our banks have been genuine helpful and extremely accommodating. Loan repayment holidays and interest rate reductions have been granted to many customers. However, when additional loans are needed to keep businesses afloat, the question every Relationship Manager will be asking is, are we just adding more liabilities to a business which is doomed to fail or are we genuinely assisting this business to survive the crisis and come out of the other end intact. It is a critical question how banks manage this process and will have serious repercussions on their profitability Post COVID 19. Post crisis will see Banks focus on preserving their customer bases. Every client who survives the crisis is an asset to the bank that will continue to pay interest on their loans which will have probably increased. Those who did not survive will be added to the pool of non-performing loans that are on the bank Balance sheets and over time written off as impairment losses. Post COVID-19 will see every bank worldwide have increased coronavirus-related provisioning on their balance sheets for future loan losses facing conditions of eroding margins, as they compete for an already reduced market of lenders. It is clear that any recovery from the crisis will be slow, and lengthy and uneven with the deadweight of Non-performing loans impacting profits and returns on capital.

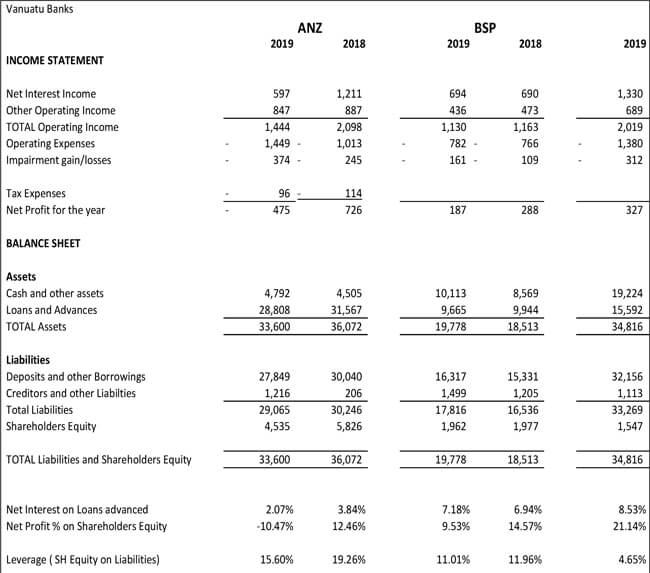

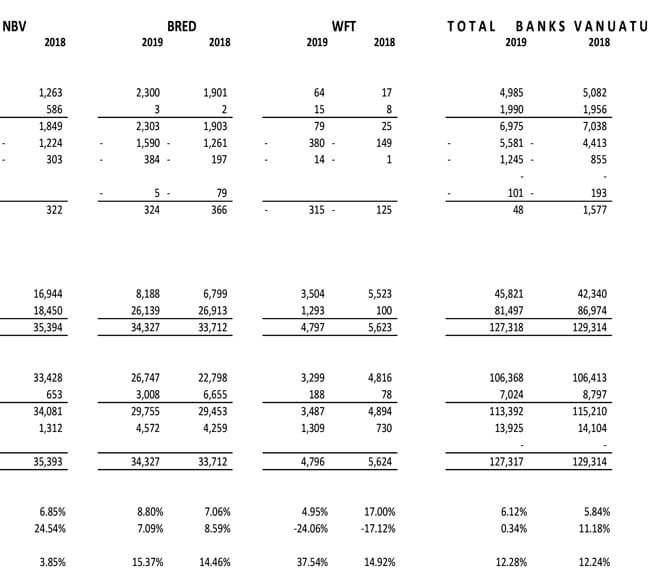

In Vanuatu, our banks have had a mixed 2019. The law requires Banks to publish their financial results each year so the VBR has had the benefit of reviewing and comparing the financial performance of our banks. In total, Vanuatu Banks generated a combined total of Vatu 48M in Net Profit 2019. This is in stark contrast to 2018 when the banks made a combined profit of Vatu 1.5BN. The 2019 results show already deteriorating business conditions as compared to 2018 with net interest income falling, increasing bad debts and increased amounts of liquidity on the balance sheets. The COVID-19 crisis will only compound an already bad situation and one Bank has already indicated that its first quarter result is worst for the same period in FY 2020. As a consequence of COVID-19, it is not expecting an improvement over the next few quarters.

When looked at separately, the banks have had very mixed results. The star performer in 2019 has been NBV which continues to generate good profits. Despite the good results, the NBV, is still highly exposed to a worsening economic crisis. Out of all the banks, the NBV has the highest amount of leverage. A high amount of non-performing loans in the Post COVID-19 years will place a lot of pressure on the banks which are highly leveraged. This is shareholders equity as a percentage of Liabilities. The NBV at the end of 2019 had Shareholders equity of 4.65% on Liabilities. In contrast to this, the newly established WanFuTeng Bank has been actively trying to grow its loan portfolio with competitive interest rates and aggressive marketing but generated loses of Vatu 315m in 2019. Its balance sheet, whilst small compared to the other banks, is not as highly leveraged as the others with Shareholders Equity of 37.54% of Liabilities, which is a good place to be in these difficult times. The ANZ in 2019 had some large one off accounting transactions which greatly affected their reported results with a Vatu 475m loss compared to a Vatu 726m profit the previous year. Whilst still profitable, BSP and BRED have both experienced falls in net interest income and profits.

As one local banker put it, if things were to worsen, any bank with good capital buffers and prudent lending policies would have more chances of surviving the current crisis. It is no different in Vanuatu. His further view is that this year there will be an increase in bad debts which will subsequently further erode banks’ capital base.

One of the sources of income for Vanuatu banks has been the purchase of Vanuatu Government Bonds. Due to the good fiscal management by the Government in past years, and revenues from passport sales, there has been very limited amounts of Bond issues by the Vanuatu Government. Combined with a reduction in lending from the Business sector, the effect on the balance sheets of the banks has been a large increase in liquidity. Money that is not being put to good use creating downward pressure on interest rates. There are suggestions that the current Economic Stabilization Package will be funded by a large bond issue that the banks can subscribe. Such a bond issue and the downstream effects of the ESP will inject much needed liquidity in to the general economy and off the balance sheets of the banks.

Under the current economic crisis our Vanuatu Banks will be in the same boat as any other banks worldwide. Most of it, on the profit and loss of their business customers.

However it is possible that this will also be reflected on their own financial statements as they struggle to operate in a lower margin and lower growth environment. Whatever the future holds, it is clear that the Banks are a critical part of the equation for how Vanuatu recovers from the current crisis.

As they say, “We are all in this Together”, Banks included.