Tax Plan

October 14, 2016 3:08 pm | Posted in Features | Share now TwitterFacebook

We took the red pen to the government’s tax proposal

The Consultation Paper for the Government’s proposed tax plan fails in many ways.

We showed it to multiple experts with significant experience in—and understanding of—Pacific island economies. We also canvassed local business owners and other stakeholders. Without exception, the plan was rejected. People characterised it as flawed, rushed and—more to the point— downright dangerous to the national economy.

But mere opposition doesn’t bring us any closer to understanding where we went wrong in this attempt. And given that we do need to take action on the impending cash flow crisis, it is important that we develop a workable strategy to deal not only with our debt servicing woes, but also with capital and operating expenditures in the coming years.

This tax plan is a poor one. It wouldn’t receive a passing mark as an undergraduate term paper. We decided the best way to deal with it, therefore, was to offer the student a critique. This isn’t comprehensive, and it’s certainly not the last word in this discussion. But we encourage the plan’s authors to take this input in the spirit of constructive criticism.

Flawed Logic

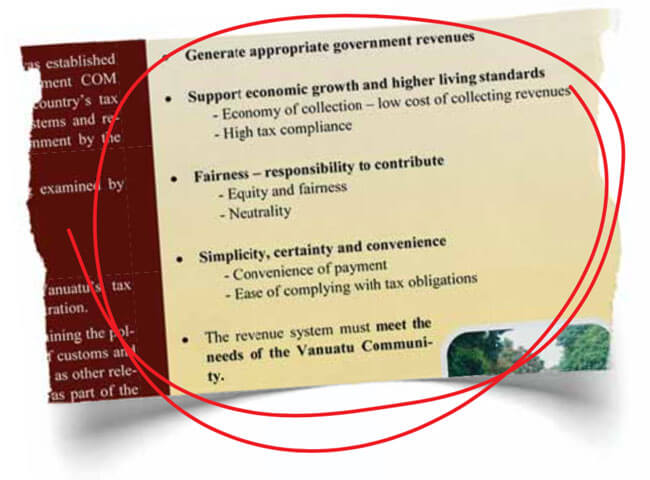

The review sets the following criteria for evaluating what alternative is best for Vanuatu:

“The revenue system” it concludes, “must meet the needs of the Vanuatu Community.”

The proposed solution fails every single one of these criteria, except arguably the first. (But that’s assuming our economy would survive it.)

The plan contains gaping holes. It states that the Review team were mandated to consider three key areas: Tax revenue; non-tax revenue; and modernisation of the tax collection process. But only one of the three pillars is considered in any detail.

Some space is devoted to modernisation of Customs and Inland Revenue, but the details just aren’t credible. Customs and Inland Revenue proposes to handle substantially the same task by creating an additional 30 positions. It expects to fund those new positions with a mere 15 million per annum in new spending.

The Australian Tax Office, for contrast, employed over 23,000 staff in 2014, with a budget of nearly $AU 3.6 billion.

The chapter dealing with non-tax revenues cites a number of well-known generalities, but fails to make a single tangible recommendation, except to say that a review would be a good idea. We… agree. A review of non-tax revenue would have been a good idea.

“The Government does not have sufficient revenue to make interest and debt repayments as well as provide essential public services, such as free basic education and health. Quality Government expenditure (including to build and maintain roads, schools, hospitals, airports, ports) is needed to achieve sustainable development and higher living standards in Vanuatu.”

Doublespeak

There are some troubling logical leaps in the material being circulated by the consultation team. Among the most memorable is their response to the question ‘why introduce income taxes’:

“The Government does not have sufficient revenue to make interest and debt repayments as well as provide essential public services, such as free basic education and health. Quality Government expenditure (including to build and maintain roads, schools, hospitals, airports, ports) is needed to achieve sustainable development and higher living standards in Vanuatu.”

The first sentence is partly true. As things stand right now, we need to come up with more revenues in order to avoid a cash flow crunch. Or, of course, we could refinance.

The second sentence is a bit of a whopper, because it implies that there will be sufficient money build and maintain a long list of new or renewed assets. That’s… unlikely.

Silence = Debt

The government promises to use the new taxes for projects, but fails even to mention its debt service requirements, the very thing that spurred this review in the first place.

Look for any mention of our debt obligations in their materials. You’ll not see much.

Even the tables they use to illustrate how they evaluated various tax thresholds and options fails to include the nearly VT 2 billion per annum that will soon be required to service our debts. To repeat: The tables used to evaluate the various tax threshold levels made no provision for additional debt payments.

This is either deception or delusion. The Director General of Finance admitted that their failure to discuss debt servicing in the document was ‘an oversight in the narrative’. But failing to mention tens of billions of vatu worth of debt isn’t just forgetting the punch line to a bad joke. It’s something far worse than that.

If we’re going to talk about the need for more government revenue, we need to be honest about it: The government is driving full steam ahead into a looming wall of debt payments. The overall amount of debt is not unacceptably high, but the fact that so much of it comes due at once will cause a cash flow crisis unless new revenues are found.

So we either need new money, or we could do what any sound financial manager would do, and refinance.

Every time debt restructuring is discussed, government officials respond that the days of debt forgiveness are past. That’s arguable, given that senior Chinese officials are on the record stating that ‘China will not force Vanuatu to pay its debts.’

But it’s also beside the point. Debt forgiveness is hardly the only option. Simply restructuring the debt into a more manageable package could completely remove the need to rush into a flawed tax regime.

Why Vanuatu is not aggressively pursuing this option with the World Bank and the ADB beggars belief.

Bad Math

Virtually every single projection in the Consultation Documents appears to be based on calculations and assumptions that are questionable at best, and outright fantasy at worst.

According to the documents, 785 corporate taxpayers will pay about VT2.2 billion in 2018. That’s an average of VT2.8 million per company. Average. As we all know, the distribution will be uneven, with a majority paying well below the average, and a choice few well above.

The government is quick to comfort people with the news that only 21% of workers will pay income tax. This means the entire burden is to be borne by roughly 6,000 people. The VT600 million initial figure means that they will pay an average of nearly VT100,000 per eligible person. Again, the distribution is very uneven. But more than half of that number, about 3,000 people, will pay only a nominal amount.

These numbers simply don’t add up. If we start making financial policy based on these projections, we will almost certainly walk ourselves straight into a major financial hole.

Pie in the Sky

As the Ronco salesman said: but wait—there’s more. Total corporate and personal income tax revenues are projected to reach VT 4.4 billion in 2018, nearly as much as we take in annually in VAT.

What will the economic impact be? We don’t know. When asked about the effect on GDP, the revenue review team said that no figures were available. Neither was inflation data. Nor were unemployment figures.

Let that sink in for a moment. We’re being asked to incur a massive rise in the cost of living with literally zero analysis on what the effect of that rise will actually be.

The very best we can do is draw some inferences from the revenue projections. Income tax revenues are projected to rise by 16% from 2018 to 2019. They are projected to rise again by 15% the following year. And by yet another 8% the following year. That’s a 39% increase in revenues in the first three years of the programme.

By 2025, the projections state that income taxes will earn the government nearly twice what VAT does today. In 2018 alone, the tax burden nearly doubles year over year. Except this time, instead of being spread across the entire consumer base, it is focused on just a few thousand people.

There is not enough magic fairy dust in the world to make that happen.

As we wrote in a recent editorial, “this is the pie in the sky that is being sold to the people of Vanuatu. We’re not saying the government is lying. We’re saying they’re dead wrong.”

The most generous interpretation we can reach is that these projections are based on wildly optimistic economic growth figures. Others aren’t so kind. One economist used a phrase involving bovine fecal matter.

Playing on pettiness

It doesn’t help when rhetoric is inserted that is sure to appeal to petty-mindedness. The Overview points out that the top 1% of workers earns 10% of the overall income. But Occupy Wall St slogans don’t apply here. Our income distribution is more equitable than in most countries. In the USA, the top 1% earned 21% of all income in 2013. And that economic pie has somewhat larger slices.

Globally, the top 1% control 48% of the world’s wealth.

And such comparisons overlook a critical factor: Vanuatu society is one of the most egalitarian in the world. There are vanishingly few high-income individuals who do not share significant portions of their wealth, not just with immediate family but with a vast web of extended family members, fellow churchgoers and tribal affiliates.

The wantok system may not be as pronounced at it is in PNG, but highly paid professionals in Vanuatu save less than most of their peers overseas.

That’s something to be proud of, but it also makes them more vulnerable to the damage that the proposed tax plan would do. Because their responsibilities stretch further than taxpayers’ in developed countries, the impact of reduced spending will be far broader. The damage will be greater, too. The most common interventions occur at times of real need: Funerals, school fees, marriages, small loans or gifts to handle short-term hardship.

Funds that get redirected to government coffers are almost certain to be the very funds that keep the village economy ticking along by providing subsistence farmers with small infusions of needful cash at key moments.

Of the top 1% of income earners, who makes out the best? The very same consultants who draft these policies. Donors and foreign consultants get off scot-free.

Sins of omission

The Consultation documents blithely leap from selling point to selling point, ignoring vast chasms of missing logic.

The government claims that it has examined numerous other options, but as this report is being written, it has not published any materials showing which options were considered, what criteria they were measured against, and why the other options failed.

There is a presentation that briefly outlines some of the other permutations they considered, such as different taxation thresholds and a VATonly solution. But the slides only describe the options and offer generalised excuses such as not generating sufficient revenues. Even such a broadbrush treatment as that has yet to make an appearance on the website.

Excise taxes—or sin taxes, as they’re more commonly known—are ignored because, according to the Consultation Paper, ‘they are not primarily imposed to raise revenue.’ That’s not true. The Philippines Government calculates sin taxes so that they offset the cost of medical care and then factors a small profit into the mix. The 2013 Health budget got a nearly 34% boost from sin taxes.

Now imagine the impact of taxes on tobacco, alcohol, refined sugars and other NCDinducing products if they went straight to improving healthcare services. A potential game-changer is left by the wayside simply because someone has assumed— wrongly—that that’s not what it’s for.

VAT increases are poohpoohed because, according to the Revenue Review FAQ, ‘As the economy grows and people’s incomes rise, they save more and consume a smaller proportion of their incomes. This means slower VAT growth.’ In a developed economy with large amounts of wealth, this is notionally true, but in Vanuatu the entire system is so small that the same people end up paying the lion’s share of the taxes no matter how you tax them.

There is very little reference to the inherent fragility of our economy, and its susceptibility to shocks. Income taxes are acknowledged to be more volatile than others, but nowhere are two and two put together to suggest that a more volatile tax base might not be ideal for an economy subject to successive shocks, such as those we just went through barely a year ago.

If we were relying on income tax to rebuild in the wake of cyclone Pam, el Niño and the recent political crisis, we would be in dire straights today.

An Impossible Task

The revenue review team proposes to begin collecting personal income tax in mid-2017, and corporate income tax six months later. That’s a pipe dream. Further, their presentations show a one-time expenditure of VT 150 million as the size of their initial investment. That’s just not true. Departmental sources have confirmed that software acquisition and upgrades alone will likely cost $AU 2 million-plus. And some independent financial analysts say the ultimate cost might run into the billions.

Even with massive donor assistance, we simply don’t have the personnel numbers or the expertise to complete this task. If the Consultation Paper has made anything clear, it’s this.

An Unfair Burden

The greatest intellectual crime committed in this proposal is the constant—and contradictory— assertion that only a few people are going to pay, but that we will somehow broaden the tax base.

If anything, the tax base is reduced—reduced, that is, to a sharp point hanging over a very few people. Among the proposed offsets to reduce the cost of doing business are the abolition of business license fees and the turnover tax. By way of justification, the consultation paper states, “turnover taxes are imposed on the gross sales of a business regardless of whether the business makes a profit or not. Fees and charges such as business licences are difficult and time consuming to comply with.”

This leaves a tax hole you could drive a truck—or at least a moderately-sized offshore finance operation—through. When business license fees were abolished in West Africa, governments lost control of business registrations, and the resulting confusion wreaked havoc on their tax collection capabilities.

And turnover taxes may be notionally less fair, but tracking and reporting is vastly easier than any income tax would be. This change would effectively pit the 30-odd extra staff at Customs and Inland Revenue against the accounting capabilities of multinational financial companies, who are nothing if not creative in tax avoidance tactics. Do they honestly think they’ll come out on top in that confrontation?

The news isn’t all bad. The revenue review team deserve an ‘A for Effort’ in the conduct of the review. They’ve taken a great deal of criticism in stride, and they’ve adjusted their efforts based on the input they’ve received. In fact, we wouldn’t have bothered with this critique if we didn’t think it would be accepted in good faith.

We understand the strictures the Revenue Review Team works within. We understand that the government faces external pressures to move on this. External studies going back to 2011 have consistently recommended the imposition of an income tax. Motivations surrounding the current move are mixed, but some are well-intended.

That doesn’t excuse such shoddy work. The proposal as it stands right now is not worthy of the current administration, which prides itself in being a more technocratic, more pragmatic and more responsive government than past incarnations.

Minor tweaks won’t save it. Short-term deferral isn’t enough to retool this troubled undertaking. We need to sit down together—public sector, private sector and civil society—and conduct a consultation similar in shape and scope to the process that brought us the National Strategic Development Plan.

Back in September, the Daily Post wrote, “Extraordinary policies require extraordinary efforts.” That is as true today as it was then.