FROM BLACKBIRDING TO BLACKLISTING

June 28, 2021 1:02 am | Posted in Features | Share now TwitterFacebook

The European Union’s Ongoing Subjugation of Vanuatu

By: Melissa Marchand

Communications Director to

Marla Dukharan

Which way is the European Union(EU) choosing with respect to it s unilateral, selective, subjective, and disproportionate application of its own tax, anti–money laundering and combating the financing of terrorism(AML/CFT) policies, on acutely vulnerable former European colonies?

While slavery was abolished in the British Empire in 1833, it was not until1904 that the heinous practice of Blackbirding-enslaving South Pacific islanders on the cotton and sugar plantations in other colonies – was brought to an end. And it is difficult not to draw the conclusion that Blackbirding was encouraged to continue in the South Pacific, well beyond the abolition of slavery, due to the remoteness and isolation from Europe and the New World. In 2021 however, FACTS DO MATTER, and the truth is not quite so easily suppressed. The Republic of Vanuatu, being such an example of a historically abused infant child of France and Britain, only gained its independence as recently as1980. Thrust into a big, bad, and fiercely‘ competitive’ new world with few life skills to rely on, Vanuatu, and indeed many other fledgling post-colonial states may have hoped, at the very least, to be given an opportunity to do just that- compete. Alas! In retrospect, it may have been naïve to not have expected to be penalized in some way for gaining independence. The EU published its first tax Blacklist of17 ‘non-cooperative jurisdictions for tax purposes’ in December 2017. Vanuatu was placed on the EU’s tax ‘Grey list’ in January 2018, and Blacklisted in March2019, where it has remained since. The EU also adopted a ‘modernized regulatory framework’ to identify ‘high risk third countries’ having strategic deficiencies in their regime on AML/CFT in 2015, and in September 2016published its first AML/CFT Blacklist including Vanuatu, where it remain seven today. It is quite the bureaucratic and statistical feat, that the EU commission was able to concoct and execute a methodology for these Blacklists, so complex, so sophisticated, so precise, and ultimately so effective in achieving their true(unstated but obvious) intent, that it produced not one, but TWO Blacklists, where NOT ONE SINGLE COUNTRY is predominantly white.

Vanuatu’s Socio-economic historical background, and current conditions

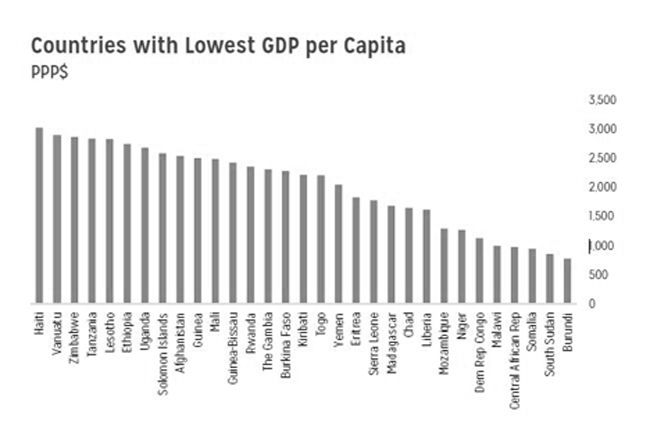

The Republic of Vanuatu is a recently graduated Least Developed Country(LDC), with a 2019 GDP per capita estimated by the IMF on a purchasing power-parity basis of USD2,889.22 – the30th lowest globally, right after Haiti’sUSD3,028, and only 9% of the GDP per capita of Greece. Because Vanuatu is located in the middle of the ‘Pacific Ring of Fire’ and directly in the centre of the Pacific cyclone belt, it is the world’s NUMBERONE most at-risk country for natural disasters, as measured by the UN World Risk Index. Vanuatu’s average annual economic losses due to natural disasters are the highest in the region, according to the Asian Development Bank. Vanuatu displays many of the typical socio-economic characteristics of vulnerable, developing, post-colonial nation. These characteristics include (to some degree) weak legal / regulatory, political, economic, and social institutional frameworks, which under pin poor governance, multi dimensional poverty, income / wealth and gender inequality, denial of basic human rights and fundamental freedoms ,environmental degradation, and political/ socio-economic instability, for example. Until December 2020, Vanuatu was classified by the UN as a LDC, which are the “poorest and weakest” low income countries with severe structural impediments, vulnerable to economic and environmental shocks.

Vanuatu graduated out of LDC status as planned in December 2020 – 40 years after its independence, despite formidable challenges, and in the middle of a global pandemic.

Upon graduation, the UN congratulated Vanuatu, stating “Repeated natural disasters, including Cyclones Pam and Harold, and recent volcanic eruptions, have decimated food stocks and forced mass displacement in Vanuatu over the last five years. And while Vanuatu only recorded its first COVID-19 case in November 2020 – much later than the rest of the world – the small island state has still been seriously impacted by the pandemic, especially by the collapse in tourism from nearby countries like Australia and New Zealand. Graduation is a major achievement but also a major challenge. Development and trading partners, and the entire UN system, must commit to providing their full support to ensure a smooth and sustainable transition for Vanuatu.

Ensuring smooth graduation requires transitioning away from LDC-specific support measures, including preferential market access for exports and access to some concessional financing instruments”.

The last point made by the UN upon graduation, is of particular relevance to the issue of Blacklisting, since it stresses the importance of transitioning away from LDC-based support systems in a manner that does not cause socio-economic instability. Having access to markets, even if no longer on a preferential basis, is crucial, and Blacklisting effectively closes off such access. Indeed, the IMF cites de-risking as a major downside risk, threatening Vanuatu’s economic recovery – “Potential reduction in correspondent banking relationships could have further adverse impact on the Vanuatu economy.”

In summary, Vanuatu is one of the world’s poorest countries, and in fact, is poorer than the poorest country in the Western Hemisphere – Haiti. we need to look more closely at one of the underlying and most fundamental challenges affecting Vanuatu – institutional weakness.

Institutions are everything

A recent study by the InterAmerican Development Bank (IDB) stated “an ample body of theoretical and applied research has shown that well-designed institutions — broadly defined as the rules that shape human interactions within a society — have a profound and enduring impact on the success of countries. The relevance of institutions for economic development has been recognized since ancient times… Countries that have strengthened the quality of their institutions have outperformed others with weak institutional frameworks, and today there is a widespread understanding that institutional quality plays an important role in shaping the patterns of prosperity and economic development around the world (Acemoglu and Robinson 2012)”.

Vanuatu was arguably also an extractive colony, but of a very different variety – apart from the extraction of agricultural output, the people of Vanuatu were also extracted – enslaved and exported to other colonies. Vanuatu lost more than half of its adult-male population on several islands at the height of Blackbirding, and the current population is deemed to be substantially lower than pre-colonial times.

This adds a whole different dimension to this particular extractive colony, because Vanuatu lost a significant proportion of its valuable, nation-building, indigenous human capital. The other indication that Vanuatu was a decidedly extractive and not a settler colony, is the fact that the population remained almost entirely indigenous, even today.

Empirical evidence shows that extractive colonies have the weakest institutional frameworks.

The IMF’s most recent assessment of Vanuatu speaks directly to this issue of institutional weakness – “Vanuatu, being a small lower-income state with limited administrative capacity, is vulnerable to corruption from gaps in governance.

These gaps leave parts of the economy either without appropriate supervision, or with excess regulation prone to bribery. Vanuatu has been strengthening its institutions through funding and technical assistance from its development partners, including the IMF and PFTAC. Recent IMF/PFTAC technical assistance has successfully focused on financial and AML/CFT legislation, tax administration and audit functions”.

While no in-depth diagnostic has yet been undertaken, it would appear that Vanuatu’s institutional framework is, by (colonial) design, not fit for its post-independence sustainable socio-economic development purpose, not yet sufficiently developed to embrace the benefits and face the challenges of graduation from LDC status, and therefore not yet equipped to navigate the international pressures to adopt and comply with the ‘Washington Consensus’ and global trade, tax, and financial regulatory norms and requirements.

The consequences of failing to support Vanuatu’s institutional strengthening to address these and other shortcomings in an already vulnerable and highly informal society, as evidenced by Blacklisting and de-risking, is economic and financial isolation – the very opposite of what Vanuatu needs, as the UN stressed upon graduation. Indeed, creating yet another pariah state is in nobody’s interest. With this better understanding of the role and primacy of institutions, Vanuatu’s expected deficiencies in this regard, and the urgency of institutional reform and strengthening, let’s take a closer look at Vanuatu’s tax and AML/CFT institutional frameworks, how various entities’ assessments of Vanuatu differ, and why.

Vanuatu’s tax framework overview and outlook

Vanuatu’s tax framework includes a VAT and excise taxes / tariffs, but no corporate tax or personal income tax. Tax administration in Vanuatu is considered to be weak – likely based on the institutional and public administration deficiencies discussed earlier.

The IMF has recommended the introduction of a personal income tax

and a corporate tax, in order to widen the tax base and earn more (predictable) fiscal revenue, and to potentially create a more progressive tax structure (VATs are generally considered to be regressive unless exemptions / zero-ratings are effective in safeguarding the lower-income group). Likewise, Vanuatu’s 2017 Revenue Review recommended that the government should engage in further fiscal reform, including introducing corporate and personal income taxes while removing inefficient taxes, reducing reliance on ECP revenues, and prioritizing the reduction of future borrowing.

But these recommendations directly contradict a 2008 Organization for Economic Cooperation and Development (OECD) study which found that corporate income taxes are THE most harmful form of taxation for economic growth: “Countries with a lower corporate income tax are likely to grow faster and attract more investment and jobs than highhigh- tax countries. Low corporate tax rates in Hungary, Ireland, and Lithuania can have a positive impact on these countries’ economic growth”.

In summary, Vanuatu’s zero corporate tax framework, which it is well within its sovereign right to adopt, is consistent with the OECD’s empirical research as growth-supportive, which is exactly what Vanuatu needs. The IMF however, is encouraging Vanuatu to implement a corporate tax AND a personal income tax, despite the empirical evidence that this could harm growth prospects, and on top of a weak tax administration system, which would achieve little anyway.

Furthermore, the push for a global minimum corporate tax rate of 15% is purely a competitive move to “prevent corporations from shifting jobs overseas” as Janet Yellen stated.

But this is precisely the kind of pressure that a poor, recently- graduated LDC with weak institutions and acute climate vulnerability, does NOT need. Instead, Vanuatu needs the international community to support its growth, allow fair access to markets for its agricultural produce and tourism, provide technical assistance to strengthen its institutions, and assistance to build climate resilience.

The Global Tax Authorities’ View on Vanuatu

The OECD1 established the Global Forum on Transparency and Exchange of Information for Tax Purposes , which now has 154 members and is recognized as the global tax policy authority. The mission of the OECD is to promote policies that will improve the economic and social well-being of people around the world. Importantly, since 2009, “no jurisdiction is currently listed as an uncooperative tax haven by the Committee on Fiscal Affairs” of the OECD.

As of 2019, Vanuatu has been classified as ‘Partially Compliant’ overall, by the Global Forum Peer review. Furthermore, despite its zero corporate tax status, Vanuatu does not appear on Tax Justice Network’s corporate tax haven index, because so little corporate tax revenue is lost in Vanuatu to domestic tax evasion, estimated at USD5.4 million annually.

Furthermore, only an estimated USD7 million is lost annually by other countries, in Vanuatu. On a global scale, this is a rounding error, of nuisance value at best.

In summary, neither the globally recognized tax policy authority, the OECD, nor the global tax watchdog, the Tax Justice Network, consider Vanuatu’s zero corporate tax structure to be inappropriate or harmful, and neither has placed Vanuatu on its list of non-cooperative jurisdictions or its tax haven index. Vanuatu’s corporate tax policy does not present a challenge internationally, nor is there any evidence to support that it is not fit for purpose domestically.

The EU appoints itself the God of Taxes

Enter the EU2 whose members are mostly also OECD members. As distinct from the OECD’s Mission which is global in nature, the goals of the EU are specific to its Members only.

The EU published its first tax Blacklist of 17 countries in December 2017. Vanuatu was placed on the EU’s tax ‘Greylist’ in January 2018, and Blacklisted in March 2019, where it has remained since.

The obvious question arises: Why should non-EU member countries be obligated to adhere to the EU Code of Conduct and other EU requirements in the first place, but especially when, as in the case of Vanuatu, they are already ‘Partially Compliant’ with the OECD’s requirements, and the OECD has not taken any punitive action?

The EU’s separate tax-haven Blacklisting assessment methodology considers not only whether the OECD’s requirements are met, but goes further to include additional requirements, including: “The country should not… go against the principles of the EU’s Code of Conduct”. Incidentally, the EU’s Code of Conduct Group, which is responsible for con-ducting much of the work that goes into constructing the Blacklist, was challenged by the Members of the European Parliament as to “whether an informal body such as the Code of Conduct Group is able or suitable to update the blacklist”.

What more could the EU justifiably want? Code of Conduct adherence apparently, but what else could possibly prompt the EU to so brazenly adopt such an unfair, opaque, if not illegal stance? Perhaps:

• The EU (ex-Germany) overall is relatively uncompetitive — Germany ran the world’s biggest current account surplus for a fourth consecutive year in 2019 at EUR258.6 billion, while nine countries recorded current account deficits (down from 11 in 2018). The EU as a bloc, therefore, is relatively internationally uncompetitive, with 40% of its current account surplus generated from 2015 to 2019 coming from Germany alone, and the bloc may be seeking to address this. But why might the EU be relatively uncompetitive?

EU corporate taxes are too high — Ranging from a low of

9% in Hungary to 34.4% in France, average EU corporate tax rates at 22.5% are higher than the global average of 21.4%.

But why are EU taxes so high?

• The EU is fiscally imprudent — by the end of 2019, EU countries in total had accumulated over EUR10.8 trillion in Government debt, equal to about 78% of EU GDP. Vanuatu’s current debt/GDP ratio stands at under 60%, and Vanuatu currently generates fiscal surpluses.

Furthermore, Vanuatu has the lowest Government expenditure as a proportion of GDP in the region, and one of the lowest in the world.

Conversely, General Government total expenditure in 2019 reached 46.1% of GDP in the Euro area. But why wouldn’t EU member states lower their fiscal expenditure, affording taxpayers lower rates?

Might is Right? The EU is a bully — instead of addressing its domestic challenges with appropriate domestic policies, the EU aims to export its problems by Blacklisting non-EU countries which dare to exercise their sovereign right to set their own domestic corporate tax rates ‘too low’, and this is how they effectively destroy the competition. Furthermore, the EU protects their own by excluding their own low-tax members from any tax-haven Blacklist. And beyond this, the EU also excludes certain non-EU low-tax jurisdictions. On what basis? Well, the EU’s methodology for ‘third country’ (non-member) inclusion in their tax-haven Blacklist clearly indicates that although there is a process for collecting data and ranking non-member countries on a Scoreboard, there is absolute subjectivity built-in to this methodology. In the first place, there is the inclusion of the criteria ‘strength of ties with the EU’ and ‘stability’, both of which have nothing to do with the ‘appropriateness’ of a country’s tax framework. After this Scoreboard is constructed, the EU member states then meet to decide completely subjectively, IF and HOW to use the Scoreboard! In other words, the EU feigns an objective, evidence-based, sophisticated (overcomplicated) methodology, only to include an escape clause, which allows EU members to completely arbitrarily include or exclude ANY country. Furthermore, the EU appears to have adopted a decidedly discriminatory stance against small (and already powerless) countries, whose combined share of global economic activity is insignificant at 1.1%, rendering the EU’s actions grossly disproportionate, in direct contravention of the EU’s own doctrine of proportionality.

Also, the (purported) essence of the tax-haven Blacklist seems to have been forgotten, as EU Members of Parliament pointed out: “By calling the EU list of tax havens ‘confusing and inefficient’, the Parliament tells it like it is.

While the list can be a good tool, member states forgot something when composing it: actual tax havens”. What a farce.

The EU is a racist institution — According to a 2017 article in the Politico, at 1% of employees, minorities are under- represented in the governance and decision-making architecture of the EU, despite accounting for 10% of the population. Possibly as a result of this, not all low-tax jurisdictions get Blacklisted by the EU — this classification is reserved only for those with predominantly non-white populations.

EU laws exclude predominantly-white EU states from appearing on the tax-haven Blacklist, despite evidence of non-adherence to their own standards and rules. The EU consistently omits its own low-tax members Hungary and Ireland (although EU Members of Parliament recently recommended “EU member states should also be screened to see if they display any characteristics of a tax haven, and those falling foul should be regarded as tax havens too”), the USA’s states of Delaware (69.2% Caucasian) and Nevada (68.1% Caucasian), and UK Overseas Territory Gibraltar (Gibraltarian 79%, other British 13.2%), among others.

The EU is overstepping its bounds by dictating the tax policy if not the ideologies of Governments and

countries beyond its membership. The EU’s tax-haven Blacklist methodology is farcical at best – it is disposable in the first place, deceitfully over-complicated, not evidence-based, not transparent, and shamefully, absolutely subjective, resulting in a Blacklist of countries that is at once completely arbitrary,

yet perfectly reveals its true malicious intent.

Vanuatu’s AML/CFT compliance framework overview

Vanuatu’s Anti-Money Laundering and Counter-Terrorism Financing Act was implemented in June 2014, and is enforced by the Financial Intelligence Unit (FIU). Vanuatu also enacted a United Nations Financial Sanctions Act in June 2017, that aims to prevent terrorism and impose prohibitions arising from UN Security Council Resolutions and domestic resolutions.

Vanuatu is also a member of the Asia-Pacific Group (APG) on Money Laundering. The mutual evaluation report (MER) of Vanuatu was adopted in July 2015, and in 2018, the follow-up report analysed the progress of Vanuatu in addressing the technical compliance deficiencies identified in its MER. APG members and observers are committed to the effective implementation and enforcement of internationally accepted standards against money laundering and the financing of terrorism, in particular the Forty Recommendations of the Financial Action Task Force (FATF).

As the only recognized global money laundering and terrorist financing watchdog, the FATF does NOT list Vanuatu as a country under ‘High Risk’ nor ‘increased monitoring’.

In June 2018, “The FATF identified jurisdictions which have strategic AML/CFT deficiencies for which they have developed an action plan with the FATF. The FATF recognized that Iraq and Vanuatu have made significant progress in improving their AML/CFT regime and will therefore no longer be subject to the FATF’s monitoring process”.

The assessments of the APG, the FATF, and the IMF, all agree that Vanuatu – despite its many challenges – has managed to implement an AML/CFT framework that is satisfactory and up to international standards and requirements. Of course, there is room for improvement, and in the dynamic world in which we live, where regulation by definition lags innovation, especially as it relates to (financial) crime, there will always be room for improvement, not just for Vanuatu, but for every nation on Earth.

Vanuatu is still relatively new to the post-colonial process of socio-economic development, which includes these necessary improvements to the AML/CFT regime, and as the IMF stated repeatedly, it is incumbent upon (Vanuatu’s colonizers in the first place, arguably) the international community and development partners, to support Vanuatu via technical assistance. How better to learn than from friends who have already walked this road?

The EU appoints itself the God of AML/CFT

Once again, enter the EU, and as distinct from the FATF’s Mission which is global in nature, the goals of the EU are specific to its Members and its Union, as follows: “Under the Anti-Money Laundering Directive (AMLD), the Commission has a legal obligation to identify high-risk third countries having strategic deficiencies in their regime on anti-money laundering (AML) and countering terrorist financing (CFT).

The objective of the EU list of high-risk third countries is to protect the Union internal market, through application of enhanced due diligence measures by obliged entities.”

The EU adopted a ‘modernised regulatory framework’ to identify ‘high-risk third countries’ having strategic deficiencies in their regime on AML/CFT in 2015, and in September 2016 published its first AML/CFT Blacklist including Vanuatu, where it remains even today.

As mentioned earlier, in June 2018, the FATF cleared Vanuatu of any deficiencies related to its AML/CFT regime, stating that Vanuatu will “no longer be subject to the FATF’s monitoring process”. Furthermore, in March 2021, the UK published its list of “high-risk third countries for the purposes of enhanced customer due diligence requirements”

and did NOT include Vanuatu.

However, in May 2020, the EU updated its list of High Risk Third Countries, and still included Vanuatu, under the same category “High-risk third countries which have provided a written high-level political commitment to address the identified deficiencies and have developed an action plan with FATF” – when the FATF, since 2018, had identified ZERO deficiencies.

In May 2020, the EU published its Revised Methodology for the Identification of High Risk Third Countries. We review and analyze the methodology for clues as to why Vanuatu is Blacklisted by the EU, and based on the evidence and the EU’s methodology, Vanuatu remains Blacklisted by the EU for AML/CFT, because of any or all of the following:

• Vanuatu is tax-haven Blacklisted by the EU (which is a completely subjective and arbitrary list as discussed earlier),

• Vanuatu is listed as an Offshore Financial Centre by the IMF (regardless of the size / insignificance of these flows),

• Vanuatu is economically insignificant to the EU (and otherwise, actually),

• Vanuatu has recently graduated from LDC status, and is perhaps now deemed to be strong enough to withstand the

pressure of EU Blacklisting,

• Vanuatu has not compiled within the 12-month timeframe with the EU’s Benchmarks,

• Vanuatu is a small, powerless, nonwhite former European colony.

The Causes and Effects of the EU’s Malicious Blacklisting of Vanuatu

There is no body or international treaty that gives the EU the legal or even moral authority to unilaterally impose separate requirements over and above the OECD and FATF, or to impose sanctions of any kind

– Blacklisting or otherwise

- on any EU non-member country. The EU’s action should therefore be considered extrajudicial in nature, given

that the FATF and the OECD are THE internationally recognized authorities on AML/CFT and Tax policy respectively — NOT the EU.

The extent of the EU’s overreach into Vanuatu’s sovereignty and the OECD’s and FATF’s territory, its grossly

disproportionate treatment of one of the world’s smallest, poorest, and most vulnerable countries on earth, its

shamefully discriminatory stance based on size and ethnicity, and ultimately, its unapologetic immorality and de facto subjugation of the people of Vanuatu, is beyond abhorrent. The consequences of being placed

on the EU’s Blacklists should not be underestimated, as they are of a socioeconomic existential magnitude for

Vanuatu. Beyond the almost irreversible reputational damage caused by Blacklisting, Banks in Europe and

North America are in effect compelled to ‘de-risk’ banks from Vanuatu and all Blacklisted jurisdictions by withdrawing or reducing correspondent banking services, and in many cases even physically exiting these jurisdictions. The withdrawal of correspondent banking services from Vanuatu is, in effect, to place a knee on the carotid artery of its economy, with socio-economic consequences that no small, poor, and highly vulnerable country can survive, especially in this pandemic. Blacklisting – especially in a country where institutions are already weak,

where there is a high level of informality in the economy, and where cash usage is high – is counterproductive (assuming the goal of Blacklisting is to reduce money laundering, terrorism financing, and tax evasion), because it leads to de-risking, which drives higher levels of informality and cash usage, even for cross border transactions. No other form of payment and settlement is more conducive to money laundering and tax evasion, than cash-based transactions. They are completely anonymous and unrecorded. So in addition to the damaging effects of Blacklisting reputationally, economically, and ultimately socially – it also increases the risk of money being laundered and taxes being evaded. Furthermore, Blacklisted countries are subject to sanctions by the EU. This is precisely what the world’s most vulnerable country to natural disasters, a recently-graduated LDC, and one of the world’s poorest countries does NOT need. In the context of the pandemic which has thrown Vanuatu into a recession, the EU’s behavior is nothing short of brutal, and indeed the EU’s Blacklists are a clear manifestation of Europeans’

long standing penchant for domination, exploitation and brutality, which evidently continues unabated even today.

For centuries, thriving European economies were built and sustained on the backs of the very colonies which are

now desperate to survive and compete in whatever limited way we can, yet the EU is seeking to destroy the ability

of these weaker states to compete by WEAPONIZING its unilaterally, disproportionately, and selectively

applied rules on tax and AML/CFT. The EU is Vanuatu’s accuser, their own expert witness, the judge, the jury, and

the executioner. By design therefore, it is impossible for Vanuatu to satisfy the EU’s ever-changing requirements.

Furthermore, if the EU’s standards and requirements on tax policy and AML/CFT evidently do not apply to EU

member states, nor to predominantly white countries small or large, nor to the EU’s powerful political and/or

economic allies, what further evidence is required to prove that not only is the EU racist and influenced by a power

criterion, but that their Blacklists are completely subjectively, selectively, disproportionately, and maliciously

constructed, and are therefore completely devoid of any shred of credibility? Evidently, we, the former European

colonies, are being held to a higher standard than our former colonizers, BY our former colonizers. We are still

denied the sovereignty to manage our domestic affairs — even in a manner similar to that of our former colonizers.

There is no precedent for this in history. It would appear that enjoying low taxes and laundering money are privileges reserved only for predominantly- white countries and their powerful allies. Non-white former colonies are meant to remain poor and subjugated, if not exploited and enslaved. When will we ever have the freedom to conduct our affairs as white and powerful countries conduct theirs? When will we ever be given the opportunity to determine our own policies, our own fate, and compete internationally on a LEVEL PLAYING FIELD?

The EU’s policies in this context represent indisputable examples of institutional racism and bullying. The EU’s action against Vanuatu is brutally disproportionate relative to its insignificant level of economic activity (including tax evasion and money laundering) versus that of EU member states and other omitted countries. There is no known effective legal or other recourse for Vanuatu to pursue to appeal for justice. And finally, the penalties being imposed on Vanuatu have the potential to damage its economy irreparably. This is nothing short of economic warfare.