VANKLIA- The NationalPayment System

November 16, 2023 12:45 am | Posted in Features | Share now TwitterFacebook

In a Press Release dated 11 September, the Reserve Bank of Vanuatu (RBV) announced, that the automated National Payments System (NPS) – VANKLIA – was live.

What is the National Payment System NPS (VANKLIA)

VANKLIA is the automated transfer system (ATS) that is used to facilitate transactions between banks in

Vanuatu. It is a clearing and settlement system that combines the functions of Real-Time Gross Settlement (RTGS) for high-value/urgent payments with those of an Automated Clearing House for Bulk/Low-value payments. It also includes a Central Security Depository (CSD).

Vanuatu stands to benefit from this new national digital payment platform significantly, making funds transfer easier and immediate, engendering faster growth of digital financial services by financial institutions and leading to more inclusive economic development in Vanuatu. The automated NPS

marks the culmination of years of work in developing this by the RBV staff establishing robust processes,

procedures, rules, and guidelines for its applications and usage.

The development and implementation of the NPS was achieved with the financial support of the International Finance Corporation (IFC) and the World Bank with Technical input from Montran Corporation. The launch of the NPS is viewed as a transformative leap forward in the payment landscape and is poised to make a significant positive impact on the banking sector.

So how does it work?

In the past, before internet banking, transactions were conducted either by cash or cheque payments. Cheque Payments were slow and cumbersome and follow a different clearing process altogether. The delays in clearing cheques is the manual processes involved in banks taking the cheques in, processing them into their systems, then physically exchanging them with the other banks where they have come

from. The other banks then process them into their own system over the next (couple of) days by teams who check those accounts for funds, decide to bounce/not bounce, before any payments are made between the banks. This process can take between 4-7 days.

When the banks introduced internet banking, it was possible to checkbalances, view transactions and make online payments to suppliers and other funds transfers both domestically and internationally. However, prior to the launch of the NPS, these transactions were still be done manually in Vanuatu.

Requests that were placed online were still being processed manually by bank personnel which meant that when an online transaction was requested, transfers to other banks would take up to 5 days to be completed. With the NPS, such transactions are now conducted through an automated system controlled by the RBV and completed within 24 hours.

Since its launch in September, the NPS has reported minor glitches. Some of the banks when initially implementing the automated system, experienced delays in processing some payments but since that time, it has been reported that the NPS is working well.

What are the benefits of the NPS

In its press release the Reserve Bank noted the following key benefits of the Automated Payment and Settlement System. These were:

Elimination of Payment System Risk: The move away from a payment system based on cash and cheques ensures that payments are irrevocable and eliminates any payment system risk in Vanuatu.

Enhanced Efficiency: The automated payment system streamlines financial transactions, reducing processing times and enhancing overall efficiency at a much lower cost between banks and eventually the bank client.

A Basis for Other E-Payment Gateways: The automated payment system provides support to other e-payment gateways in Vanuatu which is critical in the development of E-Commerce.

Greater Accessibility: The NPS makes financial services more accessible to all, and provides a sound basis for promoting greater financial inclusion across Vanuatu.

Economic Growth: By facilitating secure transactions, the NPS supports economic activities, fostering growth and development because of the greater confidence in the payment system in Vanuatu. Stability: The NPS contributes to the financial stability of Vanuatu, ensuring a robust and resilient financial ecosystem.

Global Connectivity: The NPS opens doors to global financial networks, enhancing Vanuatu’s position on the international stage.

Have the Banks Passed on the Benefits to the Consumer

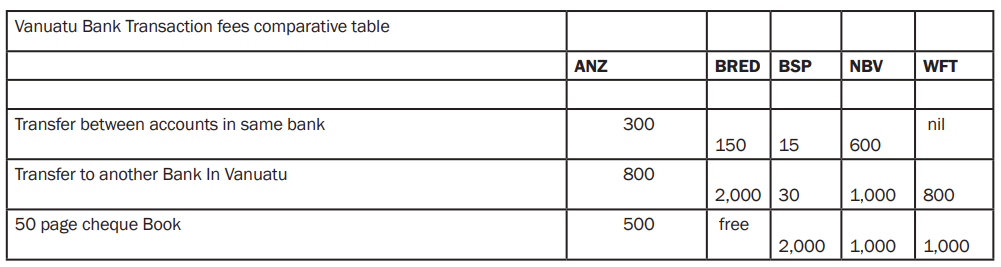

In 2022, the combined profits of Vanuatu’s Banks were approximately VT2b. Bank transaction fees contribute to the overall revenues of banks and are a significant cost to clients. As an example, with ANZ bank, for any customer requesting ANZ to make a bank to bank VUV payment they are charged VT300. The Amount charged for a transfer to another bank is VT800. The same by BRED can vary between VT1,000 – VT2,000 depending upon the amount, whether it’s a standing instruction or a one off payment.

For any Bank customer receiving a bank to bank VUV payment they are charged between VT150 to VT1,200 (depending whether it is inward TT, standing instruction or One-of requests).

Transaction fees by the Vanuatu Banks vary. The below table of fees were obtained from the fees structures from bank websites.

With the implementation of the NPS, the costs to the banks have reduced as the manual processing has now been eliminated. Sources advise that the RBV is charging the banks 10vatu for payments done at the 4 x scheduled daily payment times and 20 vatu for one-off real time payments (RTGS payments). If this is correct, then current bank margins on these transactions are very high. The ANZ have confirmed that since the launch of their own online Transactive Platform and the launch of the NPS, any online requests

that have been submitted are now free of charges. Other Banks seem to have followed suit with BRED lowering their fees for transfers to 100 vatu. Incoming transfers under the RTGS system are charged 100 vatu for each transaction. For BSP, the fee for an online transfer request to another bank is 30 vatu.

What about the Mobile Money Operators

On 21 September, the Telecommunications and Radio Communications and Broadcasting Regulator (TRBR) and the Reserve Bank of Vanuatu (RBV) announced an amendment to their existing Memorandum of Understanding (MOU). With this amendment, the RBV will assume full authority to supervise Mobile Money operators, recognizing that these operations involve financial transactions. Consequently, Mobile Money services will now be subject to regulation under the National Payment System Act. Mobile Money, a burgeoning sector in Vanuatu’s financial landscape, has been a catalyst for increased financial inclusion and accessibility. Currently, major TELCOs in Vanuatu, DIGICEL, VODAFONE and WANTOK have launched mobile payment systems for the receipt and transfer of funds on mobile phones. Vanuatu Post have also launched its own Mobile Money system. In addition, the Banks have also developed Apps that can now be downloaded on to mobile devices. This development will eventually see Mobile Money Platforms integrate with the NPS so that all banking and other financial transactions can be conducted from a smart phone with an internet connection.

What of the Future

Two months have passed since the NPS was launched. What are the bank’s future plans to pass on the benefits of cheap payments as well as the speed of the NPS? We have already seen a reduction in the fees for transfers by the ANZ and BRED.

The launch of the NPS will revolutionize the future way clients will conduct financial Transactions. Unless the banks pass on ALL the benefits of the lower costs, increased speed and efficiency of the NPS, clients will continue to rely on the use of cheques which despite the delays in manually processing, still only cost the client as low as 10 vatu per transaction. Revenue can increase by making

it more cost effective which in turn will lead to increased use of the NPS to transact.

On the business level, operating costs can be reduced, driven by less cash handling overall, time savings, as well as the gradual phasing out cheques. The National payment system is also a huge opportunity for the banks to become even more profitable by encouraging increased use of the NPS, and generating more revenue as well as reducing costs: z